The COVID-19 pandemic has thrown the American people a gigantic curveball this year. People have seen their financial situation change drastically in the months since the shutdowns began. Jobs were lost, budgets tightened, schools look different, and so many other parts of life we took for granted have changed. Amid this upheaval, you may have found that you cannot keep up with your mortgage payments the way you once did and feel like the world is closing in around you. Fortunately, in the face of this adversity, people still have options they can turn to to help them in the face of an upside-down mortgage.

The following infographic provides a brief overview of your options:

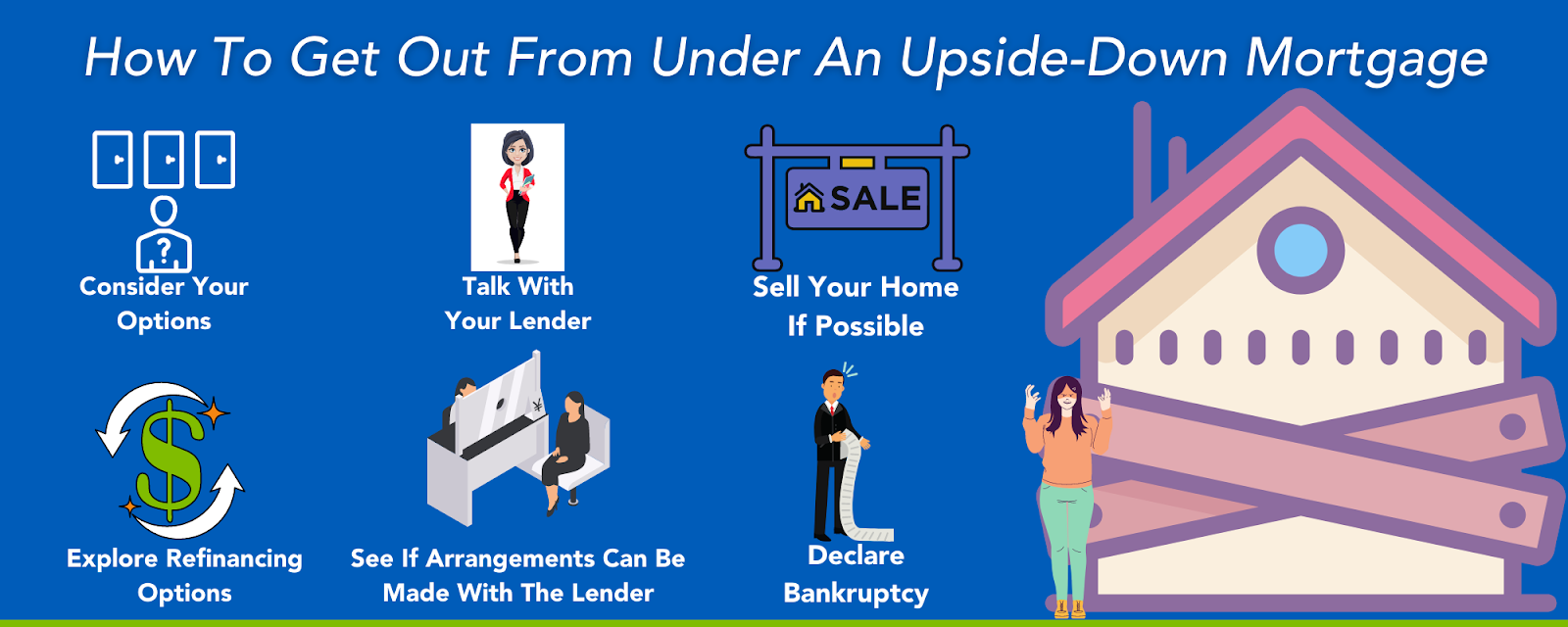

Talk Openly with Your Lender

Many people take the approach of avoiding the overdue payment notifications and hope “out of sight and out of mind” will work out in this situation. Unfortunately, that plan rarely, if ever, works out in your favor. Instead, you burn valuable time that could have been spent trying to figure out a plan of action with your lender to help your current situation. The longer you delay asking for help, the fewer options you have available.

Explore Refinancing Options

If it’s possible, refinancing your mortgage can provide the relief you need in the present. Through refinancing, you can reduce the amount in payments you make each month by renegotiating the years left on your mortgage. This path does bring with it some potentially hefty fees since you are breaking the terms of the initial mortgage, and if you have already refinanced your mortgage once, you may not have the option to do so again.

Short-Term Solutions Such As A Forbearance

Suppose you can prove that your current situation is temporary and that you can get back in good financial standing relatively quickly. In that case, you may apply for a forbearance. A forbearance is a temporary reduction or, in some cases, no payments on the mortgage for a short time. Forbearances need to be worked out with your lender and agreed upon by both parties before they can take effect. You can also talk to your lender about other temporary or permanent changes to make the situation more tenable for all parties involved.

Sell Your House

This option is easier said than done based on the current housing market conditions. If you try to sell during a downturn in the market, chances are you will not make enough in the sale to cover the remaining cost of the mortgage. In that event, a short sale or a deed in lieu of foreclosure are your only two options. Short sales happen when banks allow homeowners to sell their house for less than what is owed on their mortgage. It depends on if the lender feels if giving the ok to the short sale is in their best interest. Deed in lieu of foreclosure means that the homeowner signs the house’s deed over to the bank, and they can sell it at the price they want instead of facing foreclosure.

Declare Bankruptcy

The bankruptcy route is often the most drastic and damaging to your credit option at your disposal, but it can be effective at helping you get out from under your mortgage. Depending on which type of bankruptcy you file, you can keep your home if you have a solid plan in place to pay off the outstanding debt.

Making Sense of Your Options

Facing foreclosure during a pandemic can be an overwhelming experience. For homeowners that don’t know where to start, the Milano Realty Group can help you sort through your options and get you moving in the right direction. Contact our team to schedule an appointment today!